Created By: LPL Financial

As the morning breeze grows slightly cooler, pumpkin spice-flavored coffees return to menu boards, and the college football rankings begin to heat up, it is clear fall has arrived. September 22 marked the first day of autumn, and for capital markets this means the historically rough month of September is nearly over and the fourth quarter is around the corner. With less than five trading sessions remaining before October, stocks are on track to outperform historical averages for September, barring any major market-moving events. The S&P 500 is up 1.2% month to date, compared to the average decline of 0.7% since 1950 and declines the past four years of 4.9%, 9.3%, 4.8%, and 3.9%, which we wrote about in "Is September Seasonality a Headwind for Stocks?"

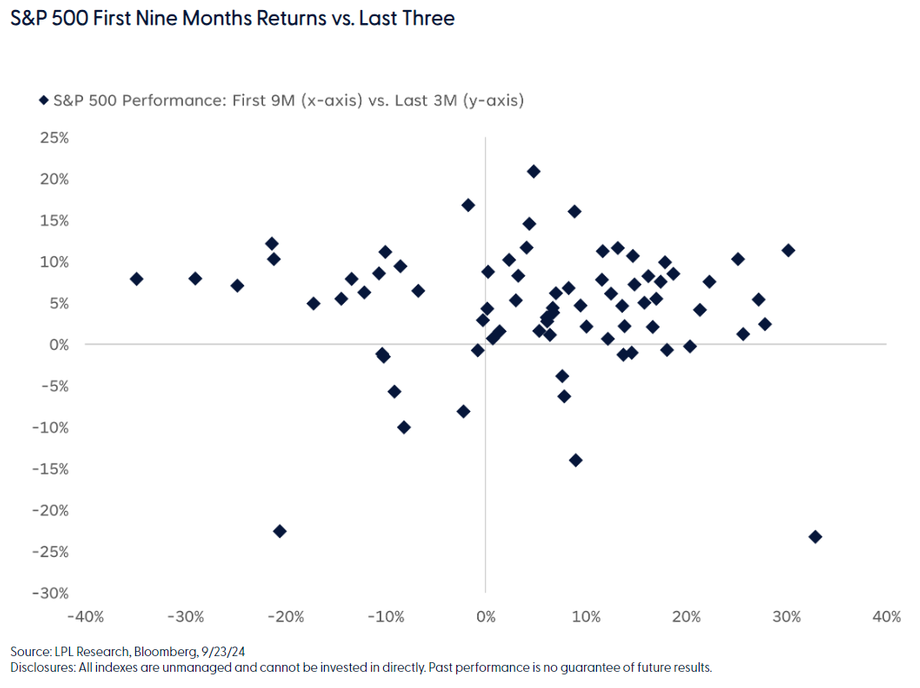

Based on historical performance for the S&P 500, strong performance and momentum in the first nine months of the year could signal more gains ahead. Over the last 75 years, the final three months of the year have resulted in negative returns only eight times when momentum was strong during the first three quarters. In four of those eight years, returns in October–December were only slightly lower, between 0% and -1.5%. The largest fourth quarter decline after positive performance through September came in 1987, which includes the infamous “Black Monday” market crash on October 19, when the S&P 500 famously shed over 20% in one day.

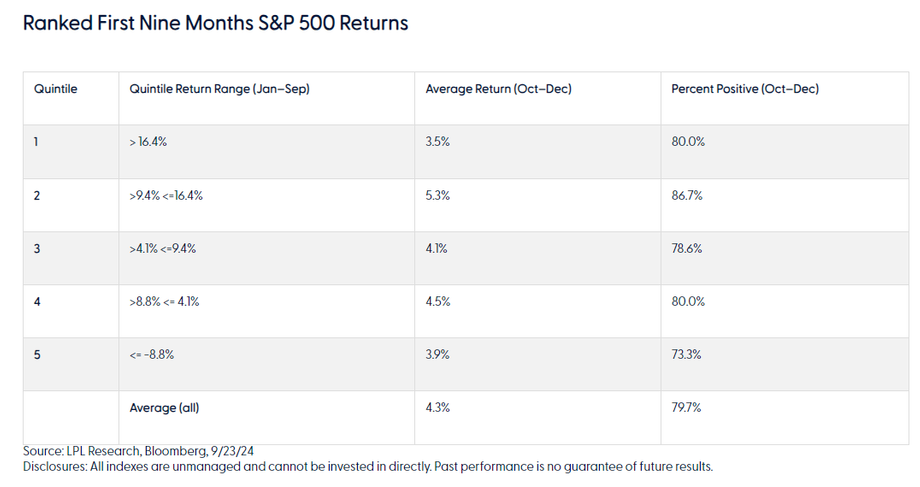

Top Quintile Performance So Far in 2024

When segmenting year-to-date returns through September into five groups, this year’s 20% gain by the S&P 500 earns a spot in the top quintile, as well as in the top 10 best for the period over the last 75 years. When returns for the first three quarters have exceeded 16.4% (top quintile), the S&P 500 has achieved positive results in the fourth quarter 80% of the time. However, the average return of 3.5% in the final quarter lags compared to the other four quintiles. After a positive first nine months, 1998 experienced the best performance with a 20.8% rally after a 4.8% gain through September. Returning to the segmented data, the highest average return for the final three months of the year has come when January–September returns fall between 9.4% and 16.4%, achieving an average return of 5.3% with positive performance 86.7% of the time.

New Records Support a Solid Fourth Quarter

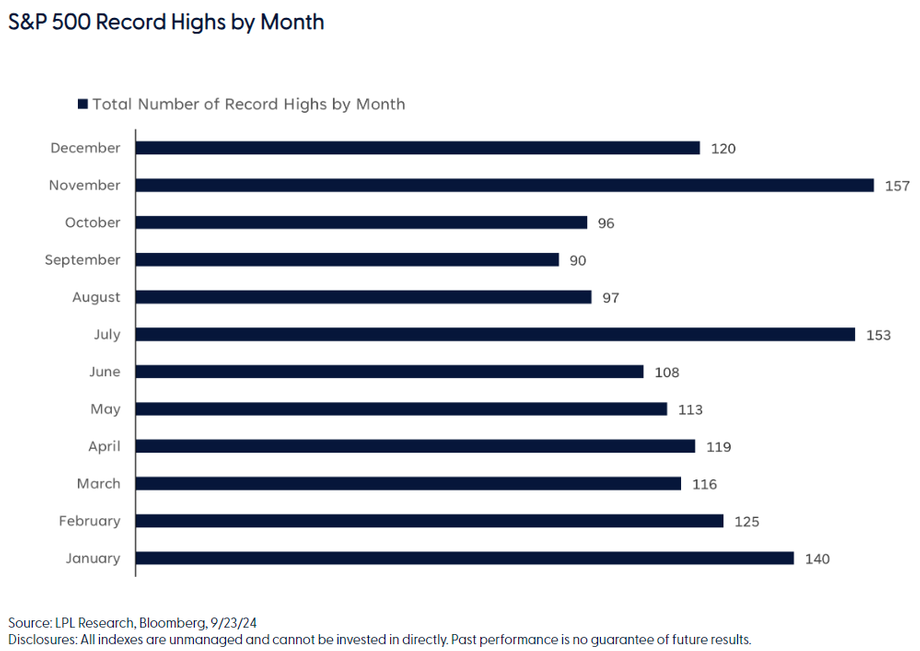

This year has been one for the history books, as the S&P 500 has secured 39 new all-time highs since the start of the new year. Most recently, on September 19, the S&P 500 climbed over the 5,700 mark following the Federal Reserve’s (Fed) jumbo half-percent rate cut, marking the first cut in four years. While it’s no secret that September is historically the worst month for stock performance, when the S&P 500 notches a new high during September, the index produced positive results in the fourth quarter 91.3% of the time. Following an all-time high in September, the average S&P 500 return in October–December is 4.8%, with 21 out of 23 years producing positive results. The strongest fourth quarter performance came amid the post-COVID rally in 2020 when the S&P returned 11.7%, while the weakest performance of -14% came in 2018, a year when the index closed the full year in the red.

Summary

Strong momentum through September, underlying positive sentiment based on soft-landing traction, and continued earnings growth have been welcomed by investors. While historical trends point to a solid likelihood of positive returns for the S&P 500 in the final three months of 2024, Fed policy decisions, a much-anticipated Presidential election, and fourth quarter earnings loom on the horizon as major market catalysts.

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its neutral stance on equities, though, with a slightly negative bias in the very short term based on the technical setup near record highs on the S&P 500, historical seasonal weakness, and political and geopolitical uncertainty. The Committee expects volatility to remain elevated in the coming months as the market waits for more clarity on the economy, elections, and a better seasonal setup.

For fixed income, the STAAC recommends a modest overweight, funded from cash, with an up-in-quality approach and benchmark-level interest rate sensitivity.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #634835